Commissions Assigned as S-Corporation Management Fees

Commissions Assigned as S-Corporation Management Fees

Many brokers and insurance agents establish an S corporation on the assumption that they can route their personal commissions as management fees through it and thereby lower their self-employment tax. The IRS is well aware of this tactic and is very actively pursuing it.

What Is This Strategy and Why Do People Use It?

The advantage is quite simple. S corporations are pass-through entities. When income comes in as a dividend rather than wages, it is not subject to self-employment tax at all. This can result in a saving of 15% or more on each dollar moved.

Therefore, some professionals send their commissions to an S corporation and record the payments as management fees. According to the documents, it is a business expense. Actually, the IRS disagrees.

Why the IRS Rejects It

The fundamental principle of taxation that comes into play here is that income is the property of the person who earned it. One cannot simply assign it to a different entity in order to alter how it is taxed.

The decisive court case that emphasizes this point is Fleischer v. Commissioner (TC Memo 2016-238). A financial advisor shifted both his LPL investment commissions and MassMutual insurance commissions into his S corporation. The IRS conducted the audit, and the Tax Court agreed with the IRS. The outcome was a deficiency notice for $41,563 of self-employment taxes over three years.

The Commission found that, because commissions were paid directly to Fleischer as an individual and not to the S corporation, they constituted personal income. Period.

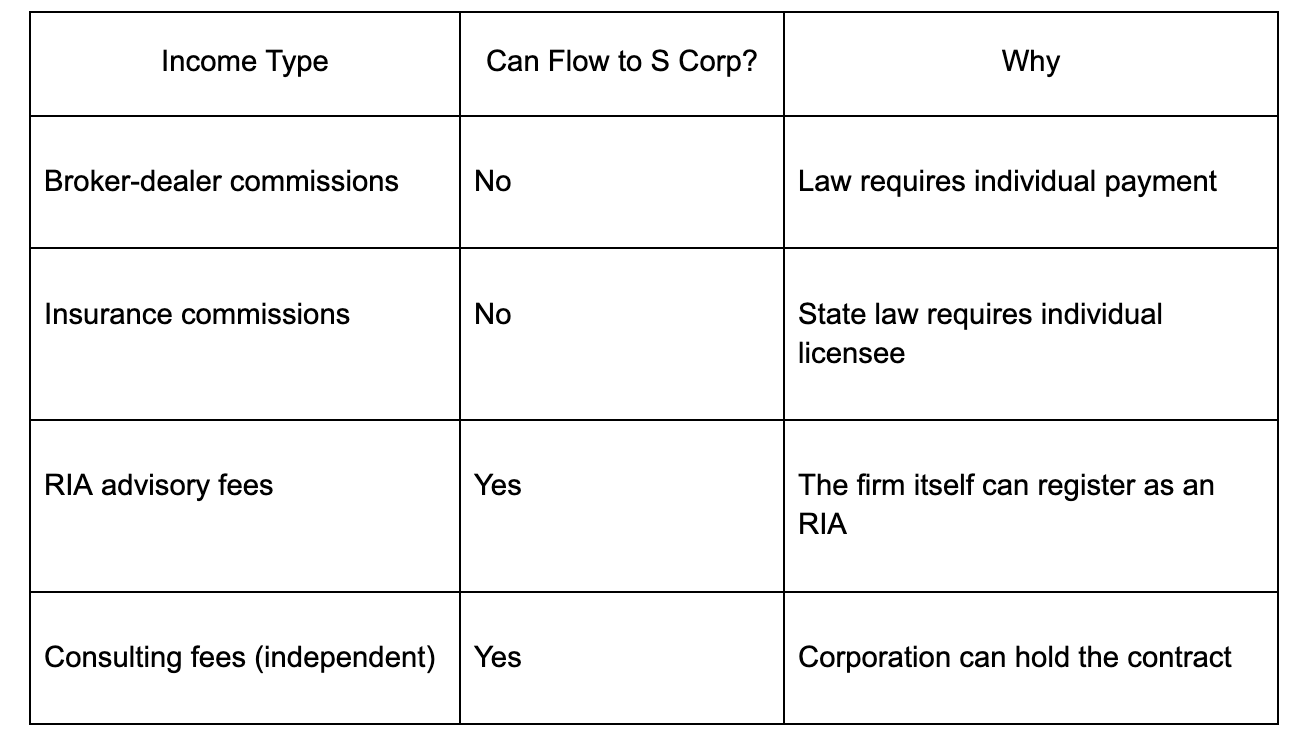

Why Commissions Cannot Legally Flow to an S Corporation

This is the point where the arrangement fails. For a corporation to legitimately recognize income, it has to be the party that was involved in the contractual relationship that generated the income.

But with broker-dealer or insurance agency commissions, this is a legal impossibility:

Under securities law, commissions have to be paid to the licensed individual.

Under state insurance laws, payments must be made directly to the individual agent.

The S corporation is not licensed and has no legal rights to such earnings.

Making a 1099-MISC out to the S corporation does not in any way validate the transaction.

The corporation was not the party that controlled the engagement. Therefore, it has no claim over the income.

What Is the Difference Between Commissions and Advisory Fees?

This is a distinction that matters a great deal.

If you operate a Registered Investment Adviser, you can register the S corporation directly as the RIA. Clients then engage and pay the firm. The firm pays you a salary. That structure is legitimate, and the IRS accepts it.

The difference is whether the corporation actually controls the client relationship and the contractual right to earn the income.

What Happens If You Get It Wrong

In that case, the IRS will turn the income back to you as an individual, and you will have to pay:

The self-employment tax for the entire amount

The interest on the outstanding balance

The possible penalties on top of that

Moreover, the Fleischer case indicated that the IRS is quite concerned with the issue. The problem was identified through random audits. Therefore, it is a real threat, regardless of how perfect the documents appear.

Conclusion

If you receive commission from a broker-dealer or insurance agency, consult a tax professional before making an attempt to reclassify that income as an S corporation. The potential savings may be very appealing, but the lawful method to get there, in fact, does not exist in most cases. The costs of getting the structure wrong are significantly higher than the sum you would have saved.